How does a homeowners association (HOA) protect the community against risks and unforeseen events? Understanding your association's master insurance policy is crucial for safeguarding the assets of the HOA and its members. This article provides a basic overview of HOA insurance, details six types of insurance coverage, highlights recent trends affecting HOA insurance coverage, and offers guidance on how to research and choose the right insurance provider effectively. With this information, HOAs can effectively manage their insurance needs, ensuring comprehensive coverage and financial well-being for their communities.

How does a homeowners association (HOA) protect the community against risks and unforeseen events? Understanding your association's master insurance policy is crucial for safeguarding the HOA's and its members' assets. This article, marking Part 1 of our insurance series, provides a basic overview of HOA insurance, details six types of insurance coverage, highlights recent trends affecting HOA insurance coverage, and offers guidance on how to research and choose the right insurance provider effectively. With this information, HOAs can effectively manage their insurance needs, ensuring comprehensive coverage and financial well-being for their communities.

- Understanding HOA Insurance: Outlining HOA insurance and its key elements, focusing on the Master Insurance Policy's role in protecting the community's assets and members.

- 5 Types of Coverage: detailing the five essential types of coverage within the master insurance policy, including property, general liability, directors and officers (D&O) liability, fidelity bond, and umbrella coverage.

- Insurance Coverage Trends: Highlighting recent shifts and trends in insurance that impact HOAs, emphasizing the importance of staying informed for effective policy management.

- Choosing the Right Provider: Offering advice on finding the most suitable insurance provider in markets with high premiums, including the importance of quote comparison and policy understanding for optimal value.

What is an HOA Master Insurance Policy?

The master insurance policy is a specialized form of coverage tailored to the collective needs of HOAs and their members, paid for by assessments collected by the HOA. Unlike individual homeowner policies, this insurance focuses on the shared aspects of the community, covering common areas and shared structures within the HOA, such as shared roofs, stairways, elevators, common hallways, and grounds. It also provides general liability coverage for the association itself, typically covering incidents within common areas but not necessarily personal liability for the actions of individual members outside of board duties.

The Master Insurance Policy serves as a financial safeguard, protecting the community's assets and the members' investments in these assets. It provides a layer of security, ensuring that in the face of unexpected events – from natural disasters to legal disputes – the HOA is prepared to recover without imposing undue financial burdens on its members. Making informed decisions about this policy is crucial for effective risk management and financial stewardship within your HOA.

5 Types of Coverage Under the Master Insurance Policy

The Master Insurance Policy encompasses a range of coverage types, each playing a crucial role in safeguarding the HOA's assets and financial stability. Understanding these coverage types is key to ensuring comprehensive protection for the HOA.

1. Property Coverage

Property coverage is the core component of the Master Insurance Policy. It covers damage to common areas and shared structures within the HOA. Regular assessment of the value of the HOA's assets ensures the coverage is adequate and reasonable. HOAs should consider the current replacement costs of these properties, factoring in the escalation in construction and repair expenses.

Tip: Refer to the HOA's reserve study, as it can provide valuable insights into the current value of the property and potential future expenses, aiding in determining adequate coverage levels. It's also important to regularly update the reserve study to reflect current costs and values.

2. General Liability Coverage

General liability protects the HOA against legal and medical costs arising from injuries or damages in common areas. With the trend towards larger settlements in liability cases[1], reviewing liability limits is more crucial than ever to prevent significant financial burdens on the HOA and its members. Consulting an insurance specialist for tailored coverage levels based on the HOA's specific risk profile is recommended.

3. Directors and Officers (D&O) Liability Coverage

D&O liability safeguards the HOA board members against personal liability due to their management decisions. Besides general liability, D&O insurance covers board negligence and breach of fiduciary duties. The increasing complexity of HOA operations and the stakes involved make D&O coverage essential. Evaluating the policy limits and coverage nature, given the potential legal costs and current legal environment, is necessary. This insurance also covers defense costs in lawsuits alleging wrongful acts by directors and officers, making understanding the exclusions and conditions of D&O policies critical.

4. Fidelity Bond Coverage

Fidelity, or crime insurance, protects against fraudulent activities or theft by employees or board members. Mandatory in California per Civil Code 5806 for associations to purchase alongside D&O insurance, it's vital for HOAs in other states to review local regulations for similar requirements[2]. The risk of incidents increases during financial strain, making strong fidelity insurance coverage a wise precaution. HOAs should ensure their policy matches the current scale of operations and financial transactions.

5. Umbrella Coverage

When a claim exceeds the HOA's general liability limits, the umbrella coverage kicks in. In the event of an accident, any additional cost after exhausting the HOA's general liability coverage will be paid using this coverage. Consider carrying umbrella coverage if your HOA provides amenities or assets that may result in liability, such as a playground or swimming pool.

Additional Coverage

Additional coverage types, such as flood insurance, earthquake insurance, or umbrella policies, might be necessary depending on the HOA's location and specific needs. Evaluating these needs involves conducting a thorough risk assessment, potentially with professional assistance, to ensure comprehensive protection against all relevant risks.

Regularly reviewing the types of coverage included under the Master Policy is essential for maintaining comprehensive HOA insurance coverage.

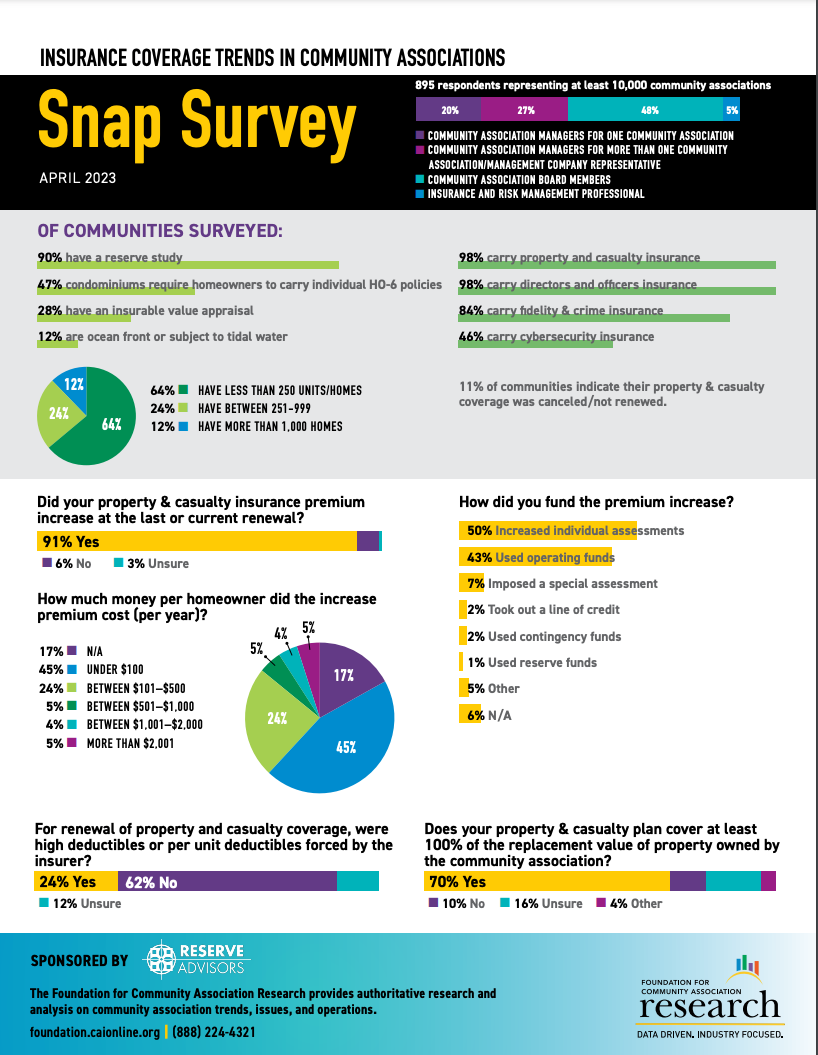

Insurance Coverage Trends

Community Associations

A recent survey by the Foundation for Community Association Research provides some insights into the insurance practices and challenges of HOAs[3].

Reserve Studies and Insurance Requirements

- 90% have a reserve study

- 47% require homeowners to carry individual insurance policies

- 28% have completed an insurable value appraisal, crucial for ensuring full property coverage

Types of Coverage

- 98% carry property insurance

- 98% carry D&O insurance

- 84% carry fidelity insurance

- 46% carry cybersecurity insurance

- 11% lost insurance coverage

Premium Increases

- 91% observed an increase in insurance premiums at their last renewal

- To offset these increases:

- 50% raised individual assessments

- 43% tapped into operating funds

- 7% resorted to special assessments

- 25% had higher or per-unit deductibles by insurers

Detailed Coverage Inclusions

- 74% have 100% replacement value of common property

- Other coverage includes:

- 56% water damage

- 54% windstorms

- 49% hail

- 41% smoke

- 41% lightning

- 35% hurricane

- 31% explosion

- 29% sprinkler malfunction/leak

- 27% earthquakes

- 26% floods

Choosing the Right Insurance Provider

By thoroughly researching potential providers and understanding the intricacies of policy terms, HOAs can make informed decisions when selecting an insurance provider for their master insurance policy. This careful approach is essential for securing a policy that fits the budget and provides comprehensive protection.

Steps for Researching and Selecting an Insurance Provider

- Gather Recommendations: Start by gathering recommendations from other HOAs, professional networks, and industry associations.

- Check Provider Credentials and Reputation: Research potential providers' credentials, financial stability, and reputation.

- Understand Specialization and Experience: Choose a provider with specific experience in HOA insurance.

- Compare Quotes and Coverage Options: Obtain and compare quotes from multiple providers.

- Clarify Coverage Details: Carefully review the coverage offered in each policy. Ensure that it aligns with the needs identified in your HOA's risk assessment and reserve study. Pay attention to coverage limits, exclusions, deductibles, and special conditions.

- Evaluate Customer Service and Claims Process: Consider the provider's reputation for customer service and handling claims efficiently. Timely handling of claims is crucial for HOAs, especially in emergencies.

- Seek Professional Advice: Consult with an insurance broker or agent who understands HOA needs. They can provide valuable advice on policy terms and help negotiate the best coverage options for your situation.

- Review Policy Annually: The insurance market is dynamic, and your HOA's needs may evolve. Make it a practice to review and compare insurance policies annually to ensure that your Master Insurance Policy continues to offer the best value and protection.

Final Thoughts

For HOAs, comprehending and managing the master insurance policy is more than a regulatory requirement; it's a strategic necessity. It requires careful attention, planning, and a dedication to grasping the subtleties of insurance coverage. By doing so, HOAs safeguard their physical assets and cultivate a secure and trusting environment within their communities. Adopting this proactive strategy is essential for dealing with the complexities of insurance and ensuring the HOA and its members' long-term prosperity.

Have you noticed an increase in your HOA insurance costs? Share your experiences and how you've addressed these changes in the comments below.

Footnotes and References

- FirstService Residential. Ask the HOA Insurance California Experts: Why are Premiums Spiking by 30%?

- California Legislative Information. Davis-Stirling §5806.

- Foundation for Community Association Research. Insurance Coverage Trends in Community Associations.